Account Relationship Structures

Fundamentally, banking services provide accounts and various mechanisms for moving money between accounts (also known as "rails"). When designing your Platform Program it is important to have a solid understanding of the relationships between the accounts required to support your use case.

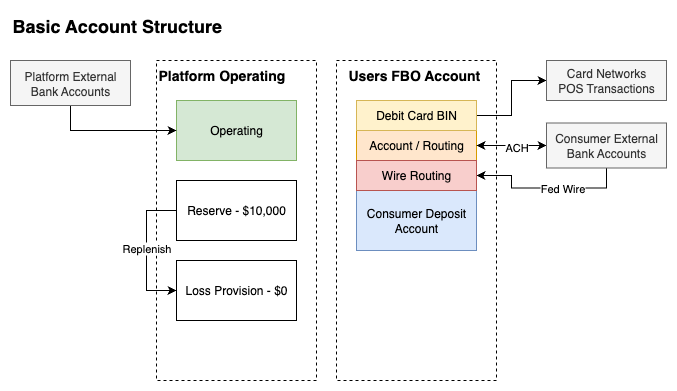

Basic Deposit Account Structure

Most Platforms provide their customers with a deposit account that has an attached Debit Card and supports ACH and Wire rails. Although broken. into two sections in the diagram below, in practice, the Platform Operating accounts and the End User deposit accounts are all maintained in a single FBO (For the Benefit Of) account at the Sponsor Bank. Only a single End User account is shown here for simplicity, but Platforms typically maintain thousands of End User accounts.

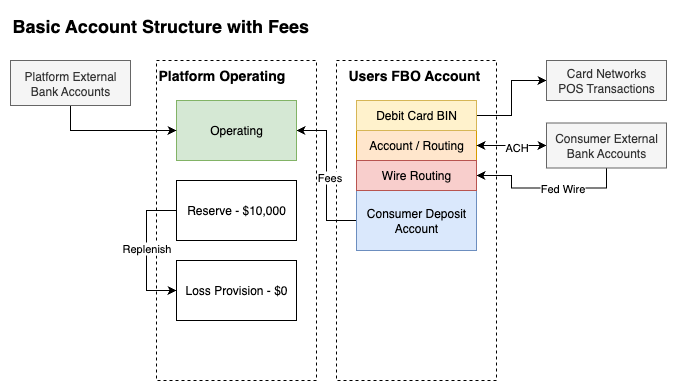

Basic Account Structure with Fees

The difference between this diagram and the one above is the diagram below indicates how fees (such as monthly membership fees) are transferred internally between the End User Deposit Account and the Platform Operating Account as required. This internal transfer takes place entirely in the FBO account at the Sponsor Bank.

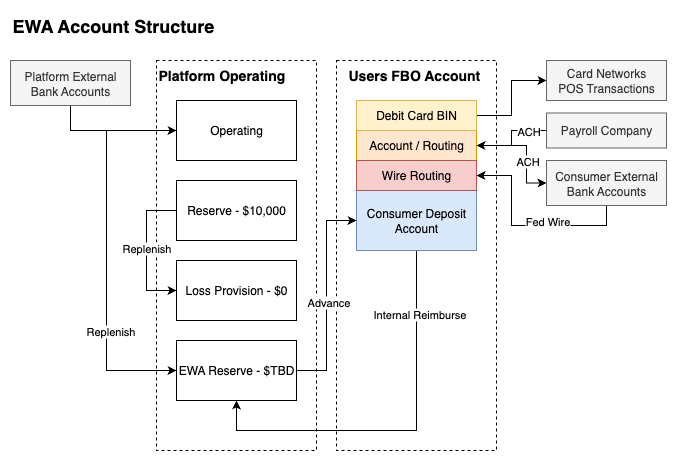

Earned Wage Access (EWA) Account Structure

Earned Wage Access is a program where the End User can request an "advance" against their future payroll deposits. The Platform has an additional EWA Reserve account to pay this advance from, and when the End User's paycheck is deposited in their Platform Deposit Account, the amount of the EWA Advance is automatically transferred back to the Platform's EWA Reserve Account.

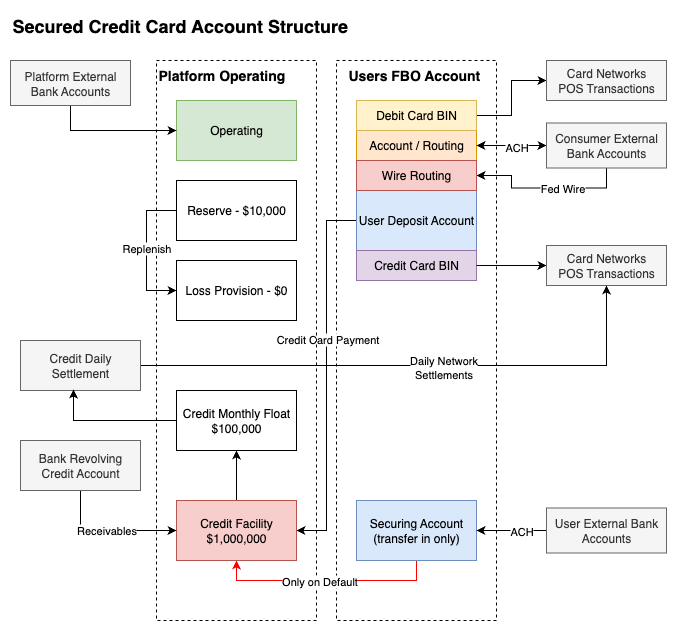

Secured Credit Card Account Structure

A Secured Credit Card is an example of a more complicated Account Relationship Structure. There is the addition of a Credit Card BIN to go with the standard Debit Card BIN. For Secured Credit Cards, the End User must fund a special Securing Account that is equal to the amount of credit that is extended to the End User. The Securing Account only allows ACH inbound transactions. Funds are only withdrawn from the Securing Account in the event that the Credit Card is in default. The Platform typically is also required to establish and fund a Credit Float Account and Credit Facility Account. These accounts facilitate the flow of credit between the End User, Platform, Sponsor Bank and Card Network (for example Visa or MasterCard).

Updated 11 months ago