Remote Deposit Capture

What is Remote Deposit Capture (RDC)?

Remote Deposit Capture (RDC) as its name implies is a method to remotely capture a physical paper check and deposit it in the bank. The way it works is that the system captures images of the front and back of the paper check, scans the image and information for potential fraud, and then performs the actual money movement using the Automated Clearing House (ACH) network.

The Check Clearing for the 21st Century Act (also called Check 21) is federal legislation that became effective in 2004 made remote deposit capture possible by allowing banks to accept check images in lieu of paper checks. Check 21 is distinct from the act of using an electronic copy of a check to make a deposit into a bank account; this process is known as remote deposit.

The check images used in remote deposit capture have to meet certain requirements, such as being a minimum number of dots per inch (DPI), not being blurry, not exceeding a certain file size, and being in a certain file format, such as JPEG. Banks also reserve the right not to accept certain types of checks by remote deposit captures, such as starter checks, traveler's checks, and checks made out to someone other than the account holder.

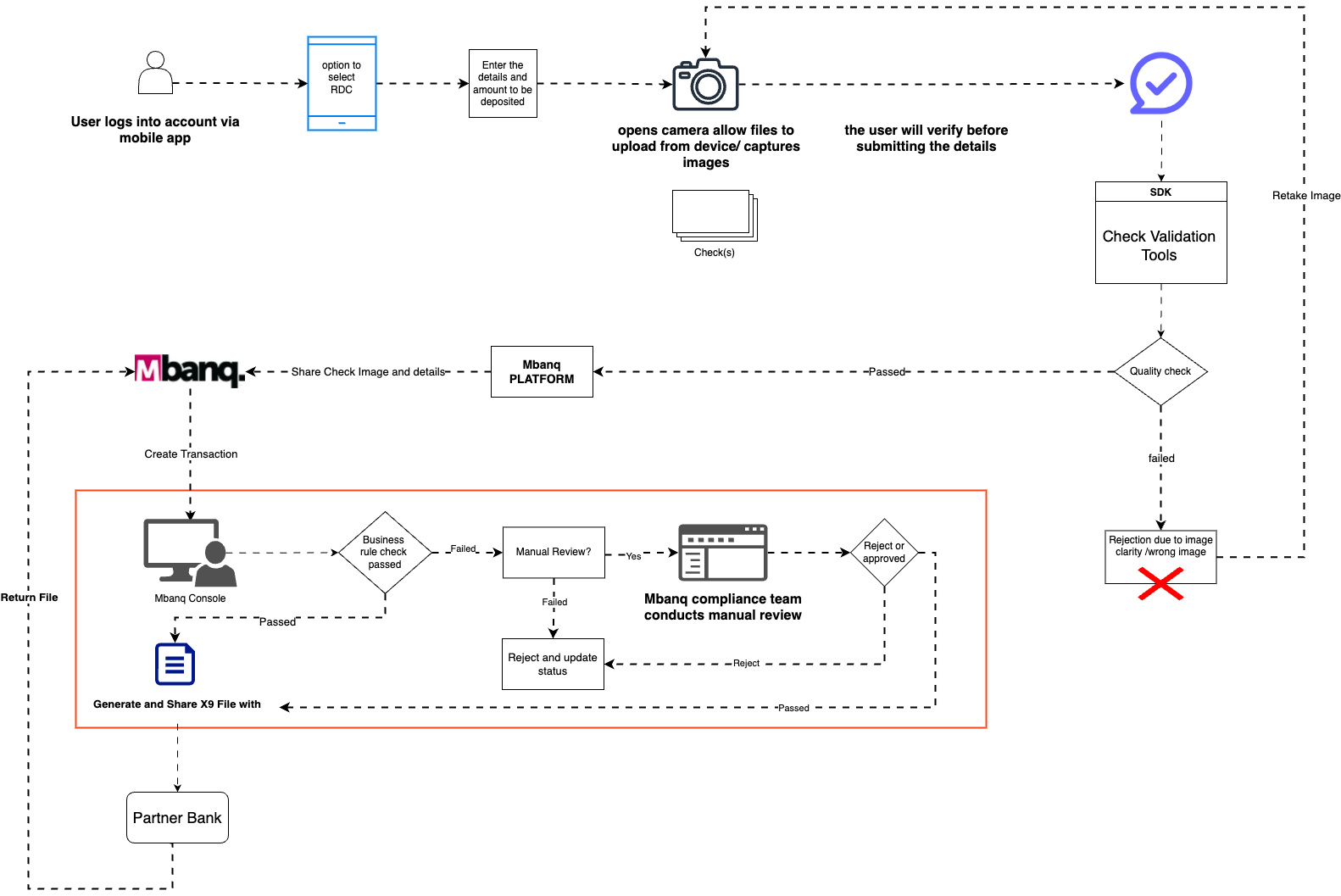

Standard RDC Flow

There are multiple steps to the RDC processing flow:

- Client endorses the check (signs on the back of the check)

- Client uses the Platform app (or Mbanq White Label app) to initiate the capture.

- Client enters key information, such as amount of check, account to be deposited in, etc.

- Client uses the app to take an image of the front of the check

- Client uses the app to take an image of the back of the check

- The app does preliminary image check for blurriness, poor cropping, etc.

- The 3rd party RDC uses OCR and data extraction to further validate checks for authenticity.

- Image and details are sent to the Mbanq back office console.

- If everything is correct, the image file is automatically processed.

- If there are detected issues, the image is sent for human review before proceeding

- Once approved, the image and check data (check number, account and routing, amount, etc.) are reformatted and stored in the X9 format.

- All the checks that are ready for processing are combined in a single X9 file and sent via SFTP to the Partner bank for processing.

- The X9 file is processed by the Partner bank through the ACH network to perform the funds transfer.

- As with any check transaction, Mbanq will report any returned check items to the Platform.

Mitigating Fraud

As with any paper check transaction, counterfeits and other fraud are always an issue. Please see RDC Risk guide for further details. One way to mitigate the damage caused by check fraud is to set velocity limits specifically for RDC transactions. Another way is to put a hold on depositing the proceeds of the check for several days to have a higher likelihood that the check will clear with good funds.

Velocity Limits

Velocity limits are set for each account and derived from account volume or past transactions.

Limits set per each RDC location:

- Single Transaction Amount – the maximum dollar amount for any single transaction

- Daily Count – number of transactions allowed per day

- Daily Amount – maximum dollar amount per day

- Period Count – the number of transactions allowed in a 14-day period

- Period Amount – maximum dollar amount within the 14-day period

Updated about 1 year ago