Card Economics

Platforms issuing cards generate revenue and incur costs through a variety of channels. A high level overview of the same is detailed below

Revenue

Interchange

In its purest form, interchange is a fee for using a network to facilitate a transaction. If you want to go somewhere by train on a railroad network, you have to pay for a ticket. If you want to talk on your mobile phone, you have to pay a fee for usage of the cellular network. In the same way, Interchange is just a fee for using the card network payment rails to process a payment.

In the distant past, you would carry around a wallet or purse full of paper money. When you went to the store to purchase something, you would take some paper money from your wallet and pay the merchant for your purchase. This worked reasonably well, but if you didn't have enough cash in your wallet, you could not make the purchase, and worse still the merchant would lose the sale. Cards were invented to solve this problem. Your bank would issue you a card, and when you presented it to the merchant, they could "run" or "swipe" it through a reader, and the issuing bank would "guarantee" the merchant that they would get paid.

How Does Interchange Work?

The primary goal is to facilitate a purchase transaction between a cardholder and a merchant. The benefit for the merchant is that the easier it is to pay for something, the more likely it is that the cardholder will buy it. The benefit for the cardholder is that they can purchase the goods and services that they need immediately without having to carry around a lot of cash in their wallet. Of course, there are costs involved in delivering this convenience, generally as the following:

- Merchant Acquirer - providing the in-store terminal equipment to "read" the card and send the transaction to the network. Often tied to an Acquiring Bank.

- Card Network - typically Visa, MasterCard, American Express or others that connect the merchant acquiring bank to the issuing bank to facilitate the flow of information and funds.

- Credit Card Processor - that aggregates all the transactions and further facilitates the flow of funds and information, including transaction authorization. Often the Credit Card Processor manages disputes as well.

- Issuing Bank - that manages accounts and cards, handles billing, and takes on the credit risk.

Some of these lines of responsibility can blur and other parties are often part of the value chain.

As card networks evolved, and given the very positive impact card convenience had on sales, it became customary for the merchant to bear the cost for facilitating card transactions. For example, if the merchant charged $100 for a good or service, at the end of the day, the merchant would only receive $97. The other $3 would go to pay the card network interchange and other fees.

Factors Determining Interchange

It would be convenient if the interchange charged on a card transaction was a flat fee like it is for sending a wire, or even a straight percentage, like 2% for all transactions, but that is not the case. Due to the fact that there are so many parties involved in facilitating the transaction and that the risk of default varies as well, interchange is highly variable and computed by a formula.

Ex: Interchange is typically a combination of a flat, per transaction fee, such as $0.10 plus a percentage of the total transaction, such as 1.5%

The following factors impact the final interchange charged for a transaction:

Network Used

Even though the Card and merchant terminal used may be branded with a particular Network logo, there are other networks that help route these transactions.

Business or Consumer

Cards issued to Businesses typically have interchange rates that are around 70 basis points higher than the interchange for a Consumer card for the exact same transaction.

Debit or Credit

Since Debit cards allow the Issuing bank to immediately deduct the purchase from your bank account, there is little to no default risk. Where as with Credit Cards the cardholder has 30 days to pay for the purchase which increases the risk of default. As a result, it is not uncommon for interchange on Debit card transactions to be a full percentage point lower than the interchange on Credit Card transactions.

Online vs. Offline In Person

As you can imagine, transacting in person with someone when you can see their face and shake their hand is much less risky than transacting with someone sight unseen online. As you would expect, this too changes the amount of the interchange fee, with riskier online transactions having higher fees.

Merchant Category

Various merchant categories have a differing amount of risk associated with them. For example online gaming, event tickets and tobacco products tend to be much riskier than purchasing groceries. To factor in this risk, the Card Networks created Merchant Category Codes (MCC) and assigned a risk level to each of them. Higher risk MCCs have higher interchange fees than lower risk MCCs.

Merchant Size

Remember it is the merchant that is paying the interchange fee. For example, $3 on a $100 purchase. As you might expect, the really large merchants, like Walmart, Amazon or Costco, have so much clout in the market, they can negotiate their own lower interchange fees from the major card networks.

Calculating Interchange for a Specific Transaction

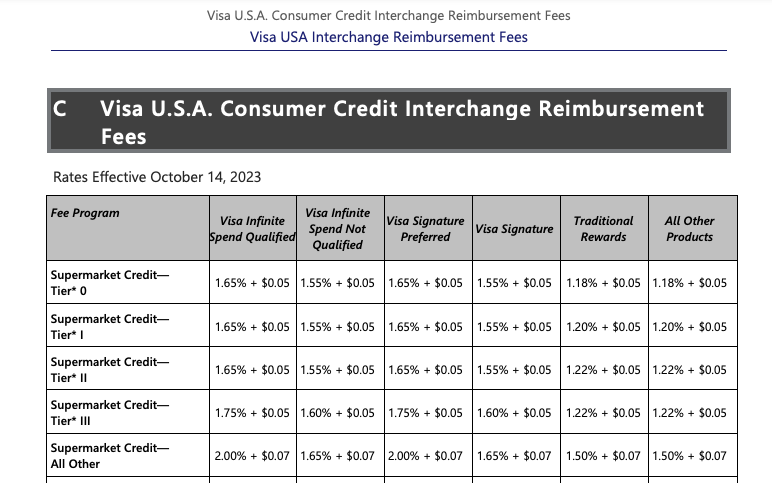

The Card Networks publish tables of interchange rates based on the above criteria. From these tables, you can calculate what the Raw Interchange should be. This link will take you to the Visa Interchange Table. Let's look at an example transaction and how we use the Visa Interchange Table to determine the Interchange fee.

Example: A consumer has a Visa Signature Credit Card and makes an in person $100 purchase at a large national grocery store chain location. From the above variables:

- Merchant Category: Supermarket

- Debit or Credit: Credit

- Business or Consumer: Consumer

- Online or In Person: In Person

- Network Used: Assume direct to Visa

- Merchant Size: Tier 1

Using this information you would go to the Consumer Credit Card Tables provided by Visa to find the table row that matches.

From the Consumer Credit Interchange table for a Tier 1 Supermarket, a consumer making a purchase with a Visa Signature card would end up with an Interchange fee of 1.55% + $0.05. So for their purchase of $100.00 the Raw Interchange would be $1.55 + $0.05 = $1.60.

Net Interchange

The Network Interchange Tables provide the data to calculate the Interchange fee associated with a purchase transaction. However, some transactions may attract a fee from the Issuer rather than earning them Interchange.

These fees are typically linked to card activity on ATM's and Foreign Networks. Examples of such fees include

- ATM Distribution Fees - Fees levied by the network on the ATM disbursements

- Special Transaction Fees - Additional fees levied by the network usually for ATM balance inquiries or declined ATM transactions

- Miscellaneous Transaction Fees - Additional fees levied by a network such as foreign transactions and ATMs

- Switch Fees - Additional fee levied by the network related to fraudulent cards. (These are rare)

The Net interchange is calculated for a particular day by subtracting all such fees from the Total Interchange earned by a card program during the period. You will find additional details on Credit Card Monthly Settlement Report

Putting It All Together

As you have seen, every single transaction a cardholder makes may be impacted by one or more of the variabilities above. That means that for business planning purposes that best that you can do is to use averages based on a wide range of purchase transactions to derive at what your interchange revenue might look like for a given portfolio of Cardholders.

Interest

For credit cards with an outstanding balance, interest income is earned until the balance is paid in full. The interest rate can vary based on the type of transaction.

- Purchase - Interest is earned once the charge is outside the Grace Period. The Grace Period is from the date and time of the purchase until the day that payment is due on the billing statement. This is typically around 30 days.

- ATM & Cash Advance - Interest is earned as soon as the money is withdrawn from the ATM or advanced online until the balance has been repaid.

Annual Fees

For credit cards and for some debit cards, the Platform can add an annual fee to the card. This is often characterized as a membership fee, initiation fee, activation fee or annual fee. Mbanq allows the Platform to specify this fee and Mbanq includes it in the activation process and on billing statements.

Costs

Sponsor Bank Costs

Typically the Client Platform will share in a portion of the Net Interchange on a monthly basis after the partner bank has taken its issuer bank share of the Net Interchange. The partner bank share percentage varies based on the partner bank and the risk profile of the Client Platform. Please refer to your contracted service agreement for details.

Network Costs

The Network charges card issuers for the ability to issue cards on their Network. The main categories of charges typically include:

Membership and BIN Maintenance Fees - The Network typically charges the Issuer a flat fee for each BIN (Bank Identification Number) ordered by the issuer.

Co-branding Fees - The Network charges the issuer for using their own or a platform's brand on Network-issued cards.

Assessment and Service Fees - The Network also charges assessment and service fees. These are typically percentage-based fees calculated on:

- The number of active cards on the Network

- The value/volume of domestic and international transactions

- Other specific services like tokenization and 3D Secure (3DS)

Processing Costs

Fees charged by the Issuing card processor for the actual processing of each transaction through the network.

Fulfillment Costs

Physical cards as well as virtual cards have a number of costs associated with producing the cards, making them accessible to the Cardholder and activating the cards. These costs can include:

- Card Design - Costs associated with the artwork design and approvals by the Partner Bank and card network.

- Card Production - Physical plastic cards have to be printed on blank cards and embossed with the credit or debit card logo. The physical card might also include EMV and near field chips.

- Custom Specialty Card Production - Platforms may opt to distinguish their brand image by offering cards with different shapes or made from exotic materials like wood, glass or metal. These cards cost more than the standard issue plastic cards.

- Card Stock - In many cases, the Platform will be required to purchase a supply of blank cards in advance to be embossed right before shipping to the Cardholder.

- Card Fulfillment - There is of course a cost associated with shipping a physical card to the cardholder's address. This can also include the costs of activating the card account and card.

- Card Replacement - From time to time the Cardholder may lose their card, or at the end of the card's useful life it is necessary to replace it.

Updated about 1 year ago