FED WIRE Transfers

API References for WIRE Payments:

What is FED Wire?

The FedWire system is a real-time gross settlement system operated by the U.S. Federal Reserve Banks. It serves as a critical infrastructure for facilitating instantaneous and secure funds transfers between participating banks. Let's dive deeper into who utilizes the FedWire system and explore the reasons behind its preference over alternative systems like ACH (Automated Clearing House):

Who Uses the FedWire System?

Financial institutions, including banks, credit unions, and other eligible entities, are the primary users of the FedWire system. These institutions leverage the system to transfer large-value funds with immediate settlement. The FedWire system's usage extends to various financial activities such as interbank transfers, securities transactions, commercial payments, and government-related payments.

Why Use the FedWire System Instead of ACH?

The choice between the FedWire system and ACH depends on the specific requirements of the payment and the desired characteristics of the transaction. Here are some reasons why financial institutions opt for the FedWire system over ACH:

-

Real-Time Settlement: The FedWire system offers immediate settlement, ensuring that funds are transferred in real time. This feature is crucial for time-sensitive transactions or when immediate availability of funds is necessary.

-

High-Value Payments: The FedWire system specializes in processing high-value payments, typically involving larger amounts of money. It provides a secure and efficient mechanism for transferring significant sums, making it suitable for corporate transactions, large-scale commercial payments, and interbank transfers.

-

Finality and Certainty: FedWire payments are final and irrevocable once processed, providing a high level of certainty and assurance to both the sender and the recipient. This characteristic makes the FedWire system ideal for situations where immediate, definitive settlement is essential.

-

Direct Transaction: Unlike ACH, which involves intermediaries and batch processing, the FedWire system facilitates direct and individual transactions between participating financial institutions. This direct connection allows for greater control, flexibility, and real-time visibility of the transaction process.

-

Regulatory and Compliance Requirements: The FedWire system adheres to stringent regulatory and compliance standards, ensuring the secure and lawful transfer of funds. This makes it particularly suitable for transactions involving sensitive financial instruments, government-related payments, and regulatory compliance purposes.

While the ACH system excels in handling high-volume, low-value transactions such as consumer payments and direct deposits, the FedWire system's real-time capabilities, finality of settlement, and focus on high-value transfers make it the preferred choice for institutions dealing with time-critical and significant financial transactions.

In summary, the FedWire system serves as a vital platform for financial institutions requiring immediate and secure funds transfers. Its real-time settlement, direct transaction capabilities, and suitability for high-value payments make it a trusted infrastructure for facilitating critical financial transactions among participating banks.

Use Cases for WIRE Payments

WIRE payments are commonly used in various scenarios, including:

- Large-scale business transactions

- International vendor payments

- Settlements between financial institutions

- High-value interbank transfers

- Real estate transactions

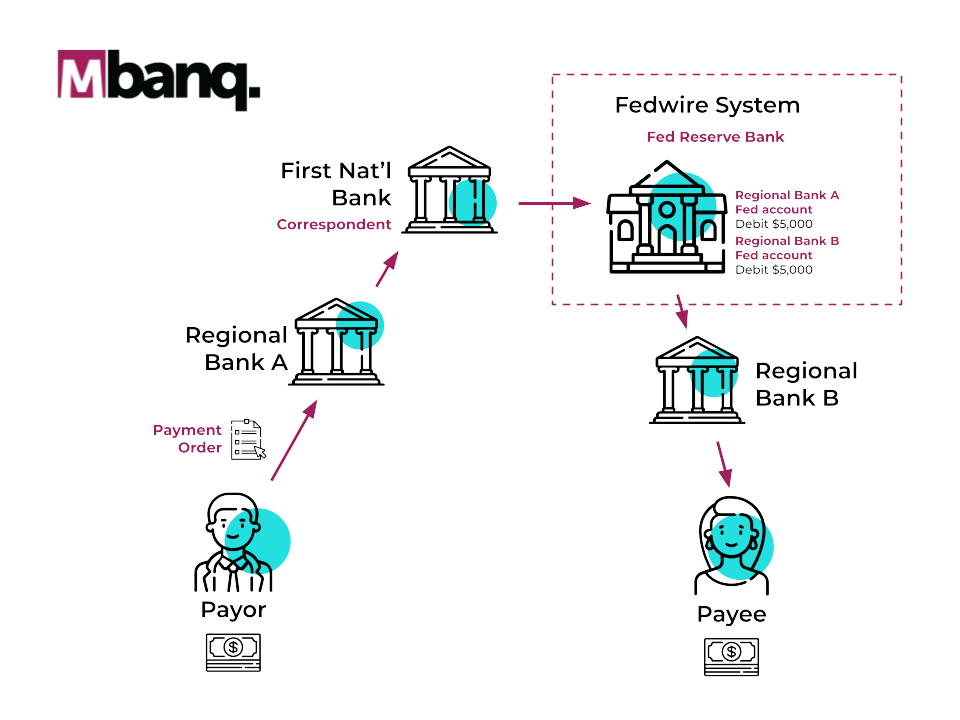

The FedWire System: How It Works

The FedWire system is a real-time gross settlement system operated by the Federal Reserve Banks, facilitating secure and efficient funds transfers between participating financial institutions. It plays a crucial role in enabling large-value payments in the United States. Let's explore how the FedWire system works and understand the key roles and processes involved:

Payor and Payee

- The payor is the individual or entity initiating the payment, i.e., the entity sending funds.

- The payee is the individual or entity receiving the funds.

Originator and Receiver

- The originator is the financial institution acting on behalf of the payor to initiate the payment order.

- The receiver is the financial institution acting on behalf of the payee to receive the funds.

Intermediary Banks

In certain cases, intermediary banks may be involved in the payment process. When the payor and payee banks are located in different Federal Reserve districts, the payment may be routed through one or more intermediary banks. These intermediary banks act as pass-through entities, simply facilitating the transfer of funds without holding any funds themselves.

Intermediary banks, also referred to as correspondent banks, play a crucial role in ensuring that payment instructions are accurately routed between the Federal Reserve Bank and the beneficiary bank. They ensure timely and accurate processing of the payment while helping to alleviate the load on the Federal Reserve Banks by handling a portion of the payment volume.

Clearing Accounts

Every financial institution participating in the FedWire system maintains a clearing account at the Federal Reserve Bank within their respective district. These clearing accounts serve as the holding accounts for funds involved in transfers between institutions.

When a financial institution initiates a payment order through the FedWire system, the funds are debited from their clearing account at the Federal Reserve Bank. Simultaneously, the funds are credited to the clearing account of the receiving institution.

Cutoff Times

Wire transfers have cutoff times because the partner banks have account reconciliation obligations with the Federal Reserve. Mbanq's FED Wire cutoff times are:

| Cutoff Time | Settlement Time |

|---|---|

| 12:00 PM PT | Same Business Day Domestic Wire transactions sent after the cutoff time will be processed the following business day. |

Updated 6 months ago