Intro to Cards

Cards Overview

Card management plays a vital role in the modern banking landscape, offering a range of financial services and empowering individuals and businesses with convenient payment solutions. This page aims to provide a comprehensive overview of MBanq's extensive card offerings, showcasing the breadth of services available to clients.

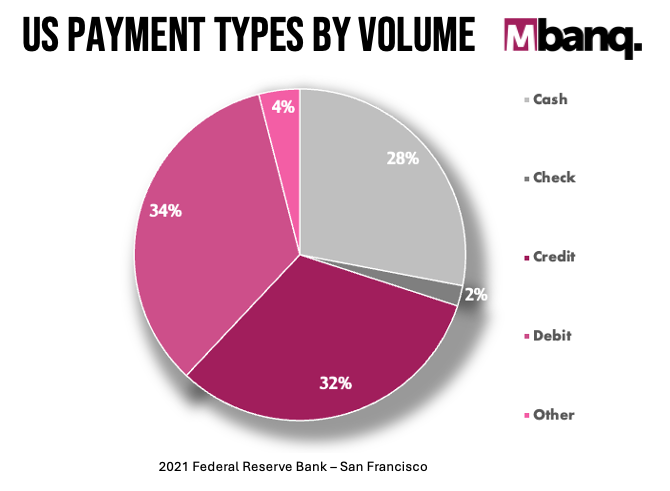

Debit cards, charge cards and credit cards make up over 65% of the payment types used by U.S. consumers. Your platform should accommodate these preferred payment methods.

Cards are not just the preferred payment method for your customers, they also can generate new revenue streams in the form of interchange and other fees for your platform. In addition, cards drive consumer engagement and retention, and can generate valuable insights into customer spending patterns. With Mbanq's Cloud CORE system and our partnership with card processing companies, we offer you a comprehensive solution to launch your credit card programs. Our experienced team will guide you through the entire process, from card art design to implementation, ensuring that your credit card offering aligns with your brand and meets industry standards.

Card Types:

Mbanq offers a wide range of card types including:

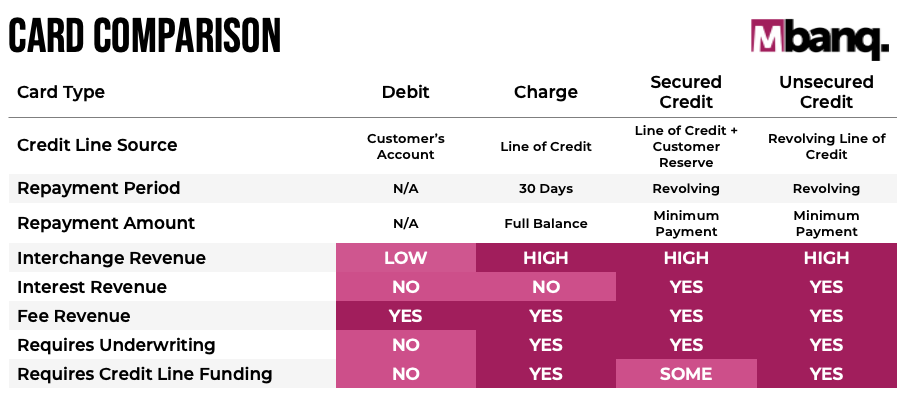

- Debit Cards - Utilize the credit card network payment rail to make payments, transfer funds, or withdraw funds from ATMs from the connected bank account. No credit is provided as the funds are immediately withdrawn.

- Revolving Credit Cards - Credit cards where the balance is not due at the end of the billing period. Typically such cards require a minimum payment which is configurable and automatically calculated by Mbanq. There are two main types of revolving credit cards, Unsecured and Secured.

- Unsecured Cards - Credit cards where the entire balance is at risk and not secured by another asset such as a cash account or collateral. See Unsecured Credit Card Guide

- Secured Cards - Credit cards where all or a portion of the open balance is secured by another asset such as a cash account. Note: the Security Deposit Account (SDA) may not be used by the cardholder to pay their current bill. See Secured Credit Card Guide

- Charge Cards - Credit cards where the entire balance is due at the end of each billing cycle. (See Charge Card Guide)

Partnerships with Card Network, Card Processor, Issuing Bank, Card Design & Print, and Shipment:

At MBanq, we understand the value of collaboration and have formed strong partnerships with key players in the card ecosystem, including renowned Card Networks, trusted Issuing Banks, and experienced providers of Card Design, Print, and Shipment services. This strategic alliance enables us to offer a robust banking platform that empowers Neo Banks and Fintech companies to launch their platforms swiftly and seamlessly, with access to all the essential services expected from a traditional bank. By harnessing the power of our partnerships, we provide the expertise and infrastructure needed to drive success in the competitive financial landscape.

Utilizing the Card Management Platform:

With MBanq's card management platform, businesses can launch a wide range of card programs, including debit cards, credit cards, corporate expense cards, and prepaid cards. Leveraging our established links and partnerships, your platform can swiftly and efficiently introduce a comprehensive debit card offering to your customers. This empowers your clients with flexible payment options, enhances their financial experience, and strengthens your fintech platform's overall value proposition.

Important Terms and Definitions

To understand the most important definitions, entities, and banks involved in the credit and debit card processing systems, it's essential to familiarize yourself with the following terms:

-

Card Network:

A card network is an organization that operates the payment network infrastructure for credit and debit cards. It connects merchants, card issuers, and acquirers, facilitating the authorization, processing, and settlement of card transactions. In this context, your card network is currently offered through VISA, one of the leading global card networks.

-

Card Processor:

A card processor, also known as a payment processor, is a company that provides the technical infrastructure and services necessary for processing card transactions. It handles functions such as transaction routing, authorization, clearing, and settlement.

-

Card Design, Printer, and Shipment:

This refers to the process of designing the physical appearance of the card, including its visual elements, branding, and personalization. Through your partnerships, you have established channels to turn your card design into a reality. This involves working with card printers who can produce the physical cards according to your specifications and facilitate the shipment of these cards directly to your customers.

-

Issuing Bank:

An issuing bank, also known as an issuer, is a financial institution that provides payment cards to customers. It is responsible for issuing the cards, managing cardholder accounts, and authorizing transactions. In your case, you have a strong partnership with an established sponsor bank that acts as the issuing bank for your platform. This partnership ensures that you can offer card services to your customers with the support and regulatory compliance provided by the sponsoring bank.

-

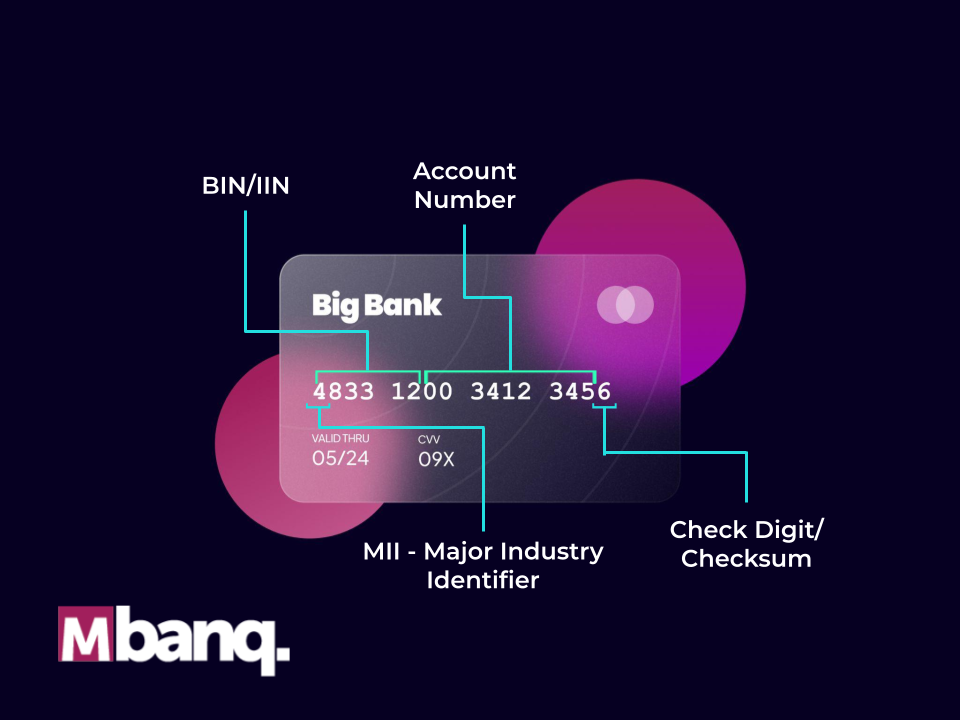

BINs (Bank Identification Numbers):

BINs are the first six digits of a payment card number. They uniquely identify the issuing bank or financial institution associated with the card. BINs are used to route transactions, validate card authenticity, and determine the card network to which the card belongs. In your case, the VISA BINs allocated to your cards signify that your cards are part of the VISA card network, ensuring compatibility and acceptance at VISA-enabled merchants.

Understanding these important terms will give you a solid foundation for comprehending the key entities, processes, and relationships involved in credit and debit card processing systems. It enables you to navigate the ecosystem and collaborate effectively with the relevant partners and stakeholders to provide card services to your customers.

Card Authorization

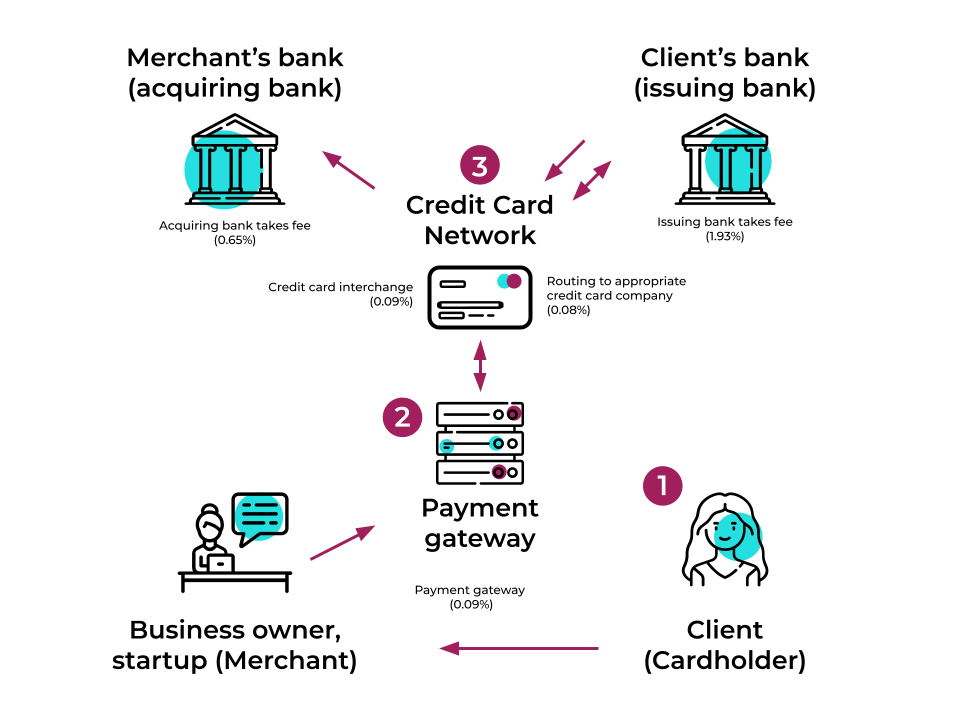

Payment card authorization is a process that allows a cardholder to make a purchase using their credit card securely. This process involves several entities, including the cardholder, merchant, acquirer, credit card network, and issuing bank. Let's break down the four steps involved in payment card authorization:

-

Cardholder pays the merchant for a purchase with a credit card:

The cardholder, also known as the customer, selects the desired goods or services from the merchant and chooses to pay using a credit card. They provide their credit card details, which typically include the card number, expiration date, and CVV code, to the merchant for payment. -

Merchant sends the card details to the acquirer:

The merchant, who is the business or seller accepting the payment, securely transmits the cardholder's credit card details to their acquirer. An acquirer is a financial institution or payment processor that establishes and maintains the merchant's account to accept card payments. The merchant forwards the card information to the acquirer for further processing. -

Acquirer forwards the credit card details to the credit card network:

The acquirer, acting as an intermediary, passes the received credit card details to the appropriate credit card network. A credit card network serves as a communication channel between the merchant, acquirer, and issuing bank. Well-known examples of credit card networks include Visa, Mastercard, American Express, and Discover. The network acts as a bridge to facilitate communication between various parties involved in the payment process. -

Credit card network requests payment authorization from the issuing bank:

The credit card network forwards the card details to the issuing bank for payment authorization. The issuing bank is the financial institution that provided the credit card to the cardholder. The bank verifies the transaction details, including the available credit limit, card validity, and potential fraud indicators. Based on this information, the issuing bank approves or declines the payment request.

During this process, the issuing bank may place a temporary hold on the cardholder's available credit limit, known as an authorization hold or pre-authorization. It ensures that the cardholder has sufficient funds or credit to cover the purchase. Once the authorization is received and approved by the issuing bank, the credit card network relays the authorization status back to the merchant via the acquirer.

Upon receiving the payment authorization, the merchant can complete the transaction, providing the goods or services to the cardholder. The actual payment will be settled later, typically in a separate process, where the merchant initiates a transfer of funds from the cardholder's account to their own account through the acquirer.

It's important to note that this step-by-step process occurs within a secure network environment, utilizing encryption and various security measures to protect the cardholder's sensitive information and prevent unauthorized access or fraud.

Important Cards API References:

Updated about 2 months ago