Intro to Transfers

Payments & Transfers with Mbanq Cloud

Transfer Overview

The key role of financial services is to manage and facilitate the movement of money from point A to point B.

Point A for example can be a person's checking account and Point B could be a merchant's checking account. Modern financial services support many different pathways between points A and B. In the industry, these are often referred to as "rails." Think of it as a network of railway tracks, and you can select which train you want to ride on to go from Point A to Point B. Some trains are slower and cheaper, perhaps taking days to go from Point A to Point B, while others are faster arriving in a matter of minutes, but of course a ticket on that train is typically more expensive.

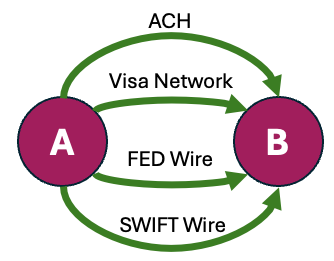

Rails

As depicted above, you could choose to move your money from Point A to Point B using any one of the available "rails." These rails include:

- ACH - Automated Clearing House: This payment rail sends "electronic checks" between two bank accounts. This is one of the cheapest methods of money movement, but it is slow. It can take two or more days for the funds to arrive at Point B. In addition, the funds are not guaranteed. If there are insufficient funds available at Point A, the transfer will "bounce." You can learn more at ACH Transfers

- Card Network - Debit or Credit Cards: This payment rail sends the funds over the Visa card network. These transactions happen nearly instantaneously and are largely guaranteed, but this speed comes at a cost, such as 1.5% of the total money moved from Point A to Point B. You can learn more at Acquiring Cards.

- FED Wire: This payment rail utilizes the electronic network that connects U.S. banks to the Federal Reserve bank. Wires are fast and the funds are guaranteed, but a ticket on this rail line can cost $25 or more. You can learn more at FED Wire Transfers.

- SWIFT Wire - Society for Worldwide Interbank Financial Telecommunication: This is a special payment rail that is used to move money between banks in different countries. Depending on the country pairs, these funds can arrive same day, next day or several days later. Like FED Wire, the funds transferred are guaranteed, but this is an expensive ticket at $40 or more. You can learn more at SWIFT Wire Transfers.

- FX Pay - This is a special purpose, real time international payment rail. Rather than using the SWIFT Wire network money is moved cross border via Money Transfer License (MTL) and then to the final destination via the local market electronic check clearing house networks. This often results in lower costs, reduced foreign currency exchange rate variations and quicker availability to funds. You can learn more at FX Pay Transfers.

- Just In Time - Just In Time payments allow for on-demand transfers, enabling quick and immediate payments to external accounts, cards, or other accountholders within the system. This flexibility ensures that time-sensitive transactions can be executed promptly, meeting the dynamic needs of businesses and individuals. Just In Time payment systems include Real Time Payments (RTP) and FED Now.

- RPPS - Mastercard's Remote Presentment and Payment Service (RPPS) is a specialized payment rail with includes remittance advice such as service provider, account number and billed amount that utilize the network to make bill payments to pre-vetted, common billers, like utility companies, landlords and the like.

Which payment rail you choose will be based on your business needs balancing speed, guarantees and cost. The choice is up to you. Mbanq Cloud provides comprehensive payment and transfer solutions for businesses and individual users. Through strategic partnerships, Mbanq Cloud enables seamless and efficient payment processing, empowering organizations to offer enhanced value-added services as their business expands.

Important Payments Guides API References:

Push vs. Pull

Transfers between Points A and B can be bidirectional. In addition, the transfer request can set the direction of the transfer.

Push Transfers

In a push transfer, Point A gives a command that funds be sent from Point A to Point B. For example, John initiates a payment of $100 to Robert. Point A has the funds and issues the instructions for the transaction. Push transactions are commonly used for bill payments.

Pull Transfers

In a pull transfer, Point A gives a command that requests funds be sent from Point B to Point A. For example, John initiates a request that Robert sends $50 to John. Point A makes the request for Point B, which has the funds, to initiate the transfer to Point A.

Pull transfers are also common in B2C subscription billing, where a Biller schedules a pull payment, pulling funds from the Subscriber's account every month.

Scheduled Payments

Scheduled Payments (another type of Push Transfer) offer the convenience of automating recurring transfers, allowing users to set up regular payment instructions. Whether it's recurring bill payments, salary disbursements, loan payments or subscription fees, the system facilitates the seamless execution of these scheduled transactions, eliminating the need for manual intervention and providing peace of mind.

Updated about 1 year ago