Card Disputes

A card dispute, is when a Cardholder challenges a charge on their bill as not being made by them. The Dispute is investigated, and if initially deemed credible, it is forwarded on to the Card Network, where a refund (also known as a chargeback) is requested. The issuing bank (or its agent) files a formal dispute on the card network, which may reverse the payment and returns the funds to the Cardholder. The ability to dispute a transaction is stipulated by government regulation. In the United States, Debit cards are regulated by Reg E whereas Credit cards are regulated under Reg Z.

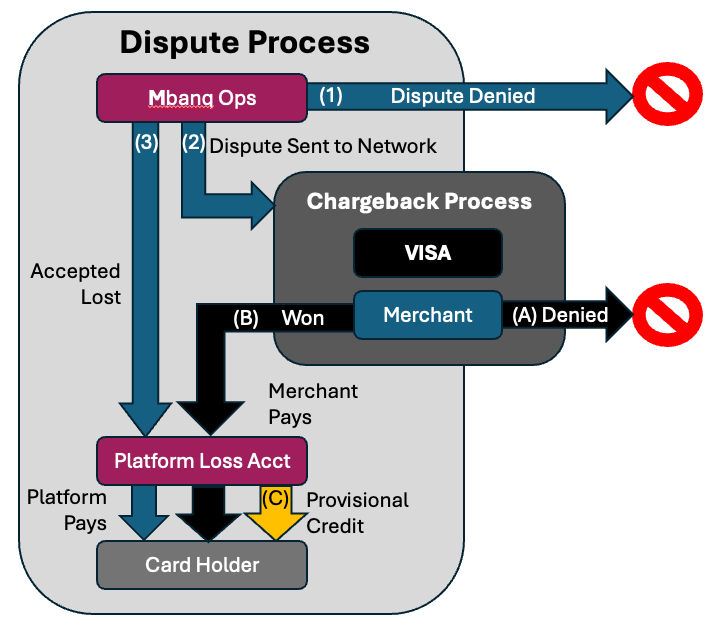

The Dispute Process

Under regulation, a card dispute must be dealt with promptly when it is received. The dispute process flow has the following main steps:

Before beginning through the flow above, the Dispute is first:

- Dispute Filed - the card holder in most cases has up to a specific number of days (for example 60) from the date of the transaction or statement to dispute the transaction. This can be done in a variety of ways, for example: via mail (as required by the regulations) or via telephone, on a website, or via the platforms app. Issuing Partner Banks can require that the request be made in writing by the Cardholder for a Provisional Credit to be given.

- Dispute Received - the Cardholder files the dispute with the issuing bank / platform.

- Dispute Logged - as soon as the dispute is received, it must be logged in a tracking system.

Once the dispute has been received and logged, Mbanq Banking Operations begins its review.

- Dispute Initial Review - the issuing bank or platform has a specific number of days within which to respond to the Cardholder that they have received the dispute and are investigating it. The issuing bank or platform my request additional information or evidence from the card holder to support their dispute claim.

- Investigation - Dispute investigations can take up to 90 days to reach resolution once submitted to the Card Network. Mbanq receives status updates from the Card Network during the investigation period.

The Mbanq Banking Operations review typically results in 3 different outcomes: (as numbered in the diagram above)

- (1) Dispute Denied - Mbanq reviews the information provided by the Cardholder and determines there is no grounds for the dispute and issues a decline.

- (2) Dispute Sent to Network - if the dispute is initially deemed valid, it is sent to the Card Network to contact the merchant as part of the Chargeback Process.

- (3) Accepted Lost - When the disputed amount is less than $25, it costs more money to send it on as a chargeback to the Card Network than to just refund the money to the consumer as a credit. The Platform is responsible for paying this refund. This can also occur for certain disputes that are more than $25 when there is not enough evidence to disprove the Card Holder's dispute claim.

Once the Dispute Claim is received by the Card Network, the Chargeback Process is initiated.

- Merchant Reviews Dispute - the merchant receives notice of the dispute via the Card Network and reviews the dispute. Based on the evidence provided, the merchant decides whether or not they will honor or deny the Chargeback request.

- (A) Chargeback Denied- After reviewing all the evidence and information the merchant can deny the Chargeback request and inform the Card Network of its decision. Refer Chargeback Lifecycle for details of the Chargeback Lifecycle

- (B) Chargeback Approved\ Dispute Won - Merchant approves the Chargeback request and refunds the funds via the Card Network

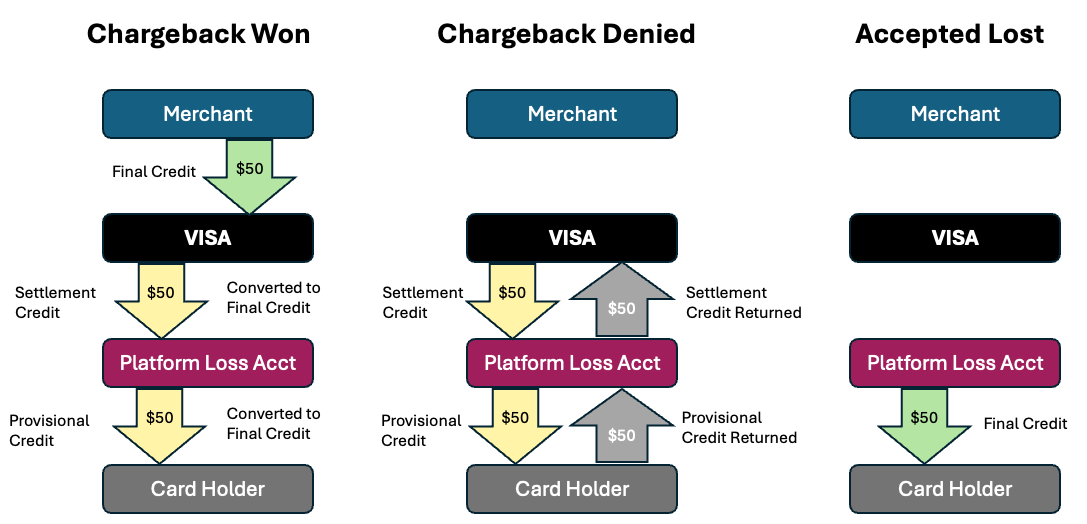

- (C) Provisional Credit - If the initial Dispute Process Investigation and the Chargeback Process take longer than the legally prescribed number of days as defined in Reg E for debit cards and Reg Z for credit cards, the Issuing Bank and Platform will be responsible for making the Card Holder whole while the investigation runs its course. In this scenario, the Issuing bank must provide the Card Holder a Provisional Credit on their account while the Dispute is being investigated. Refer Provisional Credits\

Dispute Case Closed - under regulation, the case must be resolved and closed within a specified number of days from when the dispute was first raised.

Provisional Credits

The concept of provisional credit is to make sure the Cardholder is not financially injured while the dispute investigation is proceeding. For example if a fraudulent charge on your card were to cause you to not have enough funds to make your rent or insurance payment. To mitigate this, the disputed funds are provisionally put back into the Cardholder's account while the investigation continues. Provisional Credit is a temporary credit extended to the Cardholder equal to the amount disputed. Provisional Credit is applied against the Platform Loss Provision Account. So there will be a transaction originating from your Loss Provision account, going into the user's debit card account. The issuing bank may require that requests for Provisional Credit be made in writing.

Provisional Credits post in the following timeframe for the end users:

| Age Account | Days to Post |

|---|---|

| Existing Accounts - Over 30 days | 10 Business Days |

| New Accounts - 30 days or below | 20 Business Days |

For debit cards, when a charge shows up on a Cardholder account, that money is debited from their bank account. Since that is real money, Federal Regulation (Reg E) requires that the Cardholder's account be provisionally credited for the amount of the dispute while the investigation is ongoing. If the dispute is won, the money will remain in the Cardholder's account. If the Cardholder loses the dispute, the provisional credit is returned to the Platform Loss Provision account.

For credit cards, the process is similar. When a Cardholder disputes a transaction, instead of providing provisional credit as a cash transaction, the charge is just temporarily removed from the Cardholder's bill and no interest is billed during the dispute investigation. If the Cardholder wins the dispute, the charge is permanently removed from the Cardholder's bill. If the Cardholder loses the dispute, the charged amount is added back to their bill along with any interest that may have accumulated.

Note: In all cases the funds will flow through your Platform Loss Provision account. This account will be zero balanced at the end of each month. Should rescinding provisional credit result in an overdrawn Cardholder account, you may hold the Cardholder liable for this amount. Please keep in mind that you will be ultimately responsible for any outstanding balances and negative balances are reconciled on a regular cadence from you Platform Reserve account.

Negative Balance Chargebacks

When the card account is a Debit Card or Secured Credit Card, and a Force Post transaction actually exceeds the available balance of the underlying account; the result is that the account is left with a negative balance. In these cases, the Platform can attempt a chargeback through the card network to the merchant to recover the funds. This use case can occur as part of a fraud scheme.

- Debit Card account begins with a $200 balance

- Merchant pre-authorizes for $80 purchase

- Later the merchant initiates a Force Post for an additional $150

- The balance on the account is now -$30 (negative balance)

- The Platform can issue a request via the card network to chargeback the force post amount of $150

- If the Platform is successful, the Debit Card account will be credited $150 bringing the balance to $120

For more information on credit card risks, please see our Card Payment Risk Guide.

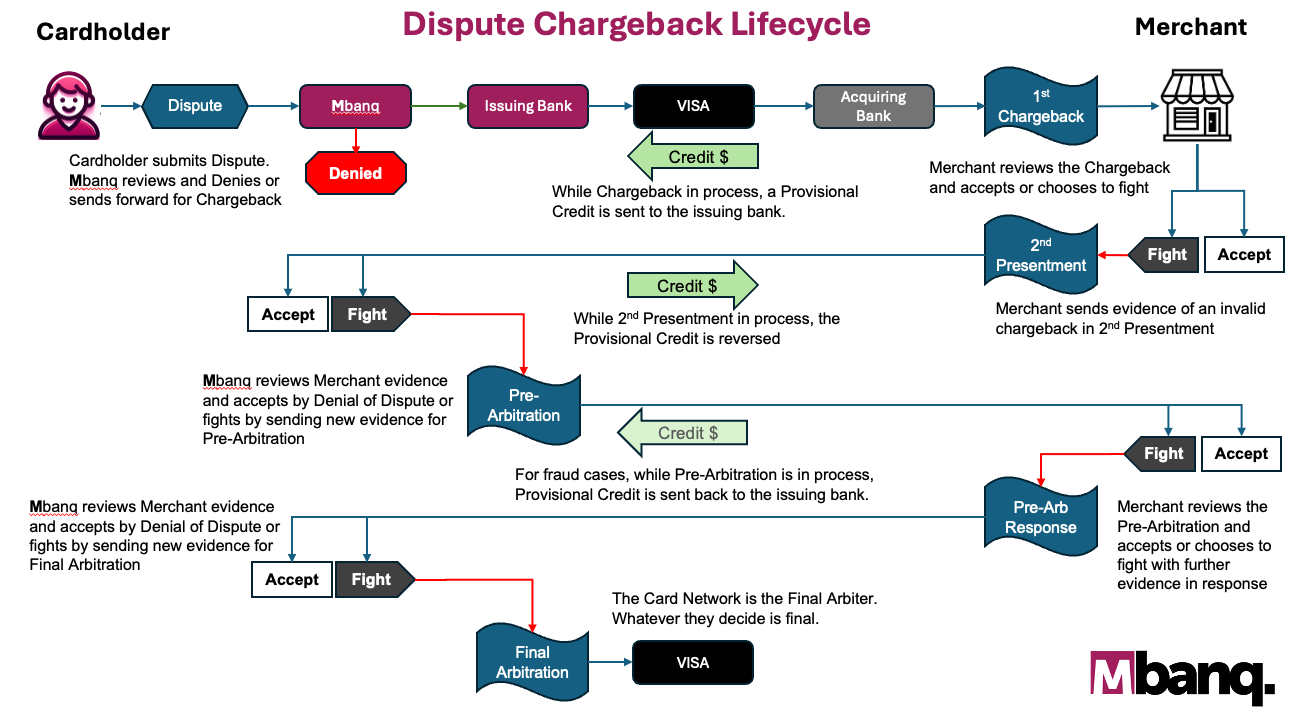

Chargeback Lifecycle

The following flow diagram depicts the various outcomes that can be expected when a dispute is submitted for chargeback. Each step is detailed below:

1st Chargeback

Timeframe20 days from the original network settlement.

Once the Mbanq Banking Operations team has reviewed the Cardholder dispute and deemed it reasonable to submit for a Card Network Chargeback, Mbanq will forward the Chargeback request through the Card Network to the Acquiring Bank and on to the Merchant for review and consideration.

Representment

Timeframe45 days from the receipt of the chargeback request.

2nd Presentment or Representment (Re-Presenting) is a right that the merchant has to present new evidence that bolsters their case that the charge on the cardholder's account is legitimate. For example, they may have discovered photographic evidence that the goods were in fact delivered, or perhaps have evidence of a separate warranty registration for the purchased product. Chargeback representment is a strictly regulated process for fighting an invalid payment card chargeback. Representment involves submitting evidence to the bank proving that a transaction was valid and that the cardholder's claim should be overturned. Merchants typically take 20 days to submit for representment, but have up to 45 days to respond. Note: If / once the card network receives a 2nd Presentment or Representment, the provisional credit provided to the Issuer at First Chargeback is reversed. This will appear as a debit on the Issuer’s account.

Merchants typically have to provide the following to make their case:

– A copy of the merchant refund/return policy.

– All copies of communication with the card holder

– Evidence that the product was delivered to the correct address

– Evidence that proves the transaction was approved and authorized by the cardholder.

– The description of the product or service

– Tracking numbers to indicate that the product was delivered.

– If the cardholder picked up the item at the merchant or at another pick-up location, provide evidence of this product delivery.

– For digital downloads, include proof of download including the IP address to which the product was delivered and the date and time of the download.

Pre-Arbitration

Timeframe45 days after the receipt of the 2nd Presentment

If the two parties cannot agree on whether or not the dispute is valid, either side can petition for arbitration. A dispute enters pre-arbitration once a merchant has represented the transaction with compelling evidence and the Platform decides to contest the re-presentment. Generally speaking, it may be prudent to submit a pre-arb for high value transactions when you believe the compelling evidence is insufficient and therefore does not prove that no error occurred. Mbanq and the Issuing Bank have up to 45 days from receipt of the 2nd Presentment or Representment to submit for Pre-Arbitration. The Acquiring Bank and Merchant have up to 45 days to respond to the Pre-Arbitration request.

Pre-arbs may be submitted for the following types of transactions:

- ATM withdrawals

- Authorization related chargebacks

- Chip liability chargebacks

- Lost/Stolen/Never received related chargebacks

Arbitration

TimeframeMerchant has 45 days to respond to the request for Pre-Arbitration before the request automatically converts to a Full Arbitration case with the Card Network.

The chargeback arbitration process works just like litigation in the legal system. The cardholder makes an allegation (the chargeback), then the merchant provides evidence in response to counter that allegation. (representment). By this stage, the parties involved—the bank, cardholder, or the merchant cannot resolve a dispute on their own. So, a representative of the card network is asked to intervene and make a judgment. Mastercard and Visa have similar regulations regarding the chargeback arbitration process. The specific steps, time frames, and terminology are different, though.

For MasterCard, in an arbitration chargeback the issuer must file for arbitration within 45 calendar days of the second presentment settlement date.

With Visa Claims Resolution rules, all Visa disputes are divided into one of two workflows. There’s an “Allocation” track for fraud and authorization issues, and a “Collaboration” track for consumer and processing errors. Visa only allows a 30-day timeframe for arbitration. The collaborative track encourages all the involved parties to work together to resolve the claim before Visa has direct involvement.

In all arbitration cases, the decision of the card network arbiter is final.

Arbitration Cost

Submitting to Arbitration can become quite costly should you lose the case. It is important to weigh the costs against the potential benefits before submitting Arbitration. We recommend establishing a de minimis transaction amount to help prevent undue costs.

Timeline

| Stage | Activity | Time | Elapsed Time |

|---|---|---|---|

| Dispute | Cardholder Disputes Charge | 120 days | 120 days |

| 1st Chargeback | Merchant Reviews First Chargeback Request | 45 days | 165 days |

| 2nd Presentment | Issuing Bank (and Mbanq) Review Merchant 2nd Presentment / Representment | 45 days | 210 days |

| Pre-Arbitration | Merchant Reviews Pre-Arbitration Request | 45 days | 255 days |

| Arbitration | Issuing Bank (and Mbanq) Submit for Final Arbitration with Card Network | 45 days | 300 days |

Resolution

The investigation will conclude when we receive the final response from the merchant or network involved in the processing of the transaction. Once the investigation has been completed, we will notify the card holder within 3 business days with its final decision based on the results of the chargeback.

Updated about 1 year ago