Intro to Credit and Lending

In capitalist economies, one of the main functions of financial institutions is to make best use of the money in the system. Simplistically, banks take in monetary deposits from one group of people and then lend it to another group of people charging them interest for the loan. The interest paid by the borrower is then paid back to the depositors as earned interest. In this way, money is constantly put to use.

Credit and Lending

Credit and lending involves allowing people to borrow money for a period of time. This could be as short as a few days or a month as is the case with credit cards and Buy Now Pay Later (BNPL) purchases, or as long as many years as in the case of term loans, automobile loans and mortgages. Regardless of the time frame, the core elements are basically the same:

- Underwriting - is the process of determining the level of risk the borrower represents and the likelihood that they will return the money they have borrowed.

- Principal - the amount of money being borrowed or credit extended.

- Term - the amount of time the borrow has agreed to pay back the money that they have borrowed.

- Interest - the fee that the borrower pays to borrow the money. This could be periodic, such as monthly, or a single amount or fee. To make it easier to compare offers of credit, interest, regardless of the time frame, is expressed as the equivalent Annual Percentage Rate (APR) that is the percentage rate that the interest would be over a year.

- Capital Source - for people to borrow money, someone has to have money for them to borrow. This is the source of capital. This can be a bank or credit union, but can also be an independent investment company.

- Capital Risk - when a person lends money, there is always the possibility that the borrower will not return it or pay it back. This is known in the industry as a Default. Someone has to assume this financial risk. Again, it could be the source of the capital, but it could also be insured by other means such as with a pledge of collateral.

Credit and Lending Types

Through the centuries, people have invented all kinds of schemes for lending money to people in need of additional capital. Mbanq supports a wide variety of credit and lending products including:

Credit Cards

Allows users to borrow money for a short period of time, typically to make purchases. For more information, please see the Intro to Cards. Mbanq supported credit card types include:

Unsecured Revolving Credit Cards

A credit product where the cardholder borrows funds primarily for purchases, with the ability to roll over the amount due month by month, paying interest on the unpaid principal balance. The capital source assumes the default risk. For more information, please see Unsecured Credit Cards.

Secured Revolving Credit Cards

A credit product where the cardholder borrows funds primarily for purchases, with the ability to roll over the amount due month by month, paying interest on the unpaid principal balance. The borrower puts up a security deposit that acts as a form of collateral to cover the risk of default. For more information, please see Secured Credit Cards.

Charge Card

A credit product where the cardholder borrows funds primarily for purchases; however, with a charge card the borrower must pay the full amount borrowed at the end of the billing period. (They cannot roll it over to the next month.) For more information, please see Charge Cards.

Loans

Loans typically have terms longer than 30 days and are often used for other purposes in addition to purchases. Mbanq supports a variety of loan products including:

Unsecured Term Loans

Unsecured Term Loans allow the borrower to borrow money for a set period of time without putting up any form of collateral or security to mitigate the loss in the event of a default. For more information, please see Loans.

Secured Term Loans

Secured Term Loans allow the borrower to borrow money for a set period of time, but protect the lender by mitigating the impact of a future default through the pledge of collateral or security deposit. These would include automobile loans and mortgages. For more information, please see Loans.

Buy Now Pay Later (BNPL)

Is a somewhat recent financial product innovation. In the past, retailers would offer "lay-away" plans where the retailer would hold the goods you wish to purchase, while you make payments on a regular basis until the product is paid for, at which point the retailer would release the product to you. Buy Now Pay Later flips this. The retailer allows you to take home the merchandise and then gives you a set number of weeks to pay the full price of the purchase, typically in 4 installments.

Regulation Z

Extending credit and lending to consumers is primarily regulated by the Truth in Lending Act, or TILA, also known as Regulation Z or Reg Z. The law requires lenders to disclose information about all charges and fees associated with a loan or extension of credit. This 1968 federal law was created to promote honesty and clarity by requiring lenders to disclose terms and costs of consumer credit. The full text of the regulation can be found here. Key elements of Reg Z include:

- Expressing interest as an annual percentage rate

- Credit card and mortgage closing disclosures

- Mortgage loan appraisal and servicing rules

- Expectations regarding recurring statements and the type of information that a financial institution or company must clearly communicate to consumers.

- Ensure that lenders provide meaningful disclosures to borrowers, using terminology that consumers can understand.

- Requiring lenders to provide written information about interest rates, and all fees and finance charges associated with a loan or credit card.

- Requiring lenders to disclose the maximum interest rate upfront on variable-interest loans backed by the borrower’s home.

- Prohibiting credit card issuers from opening a credit card account for a consumer, or even increasing a credit card’s limit, without first evaluating the consumer’s ability to make required payments under the terms of the account.

- Protecting consumers from unfair billing practices, including requiring that there be procedures in place to address billing errors on credit cards such as mathematical mistakes or incorrect or unauthorized charges.

- Requiring lenders to provide monthly billing statements to borrowers and notices if the loan’s terms have changed.

- Informing potential borrowers as to why their application for credit was denied, and if it was based on third-party information, how to contact that provider if they believe the data is not accurate.

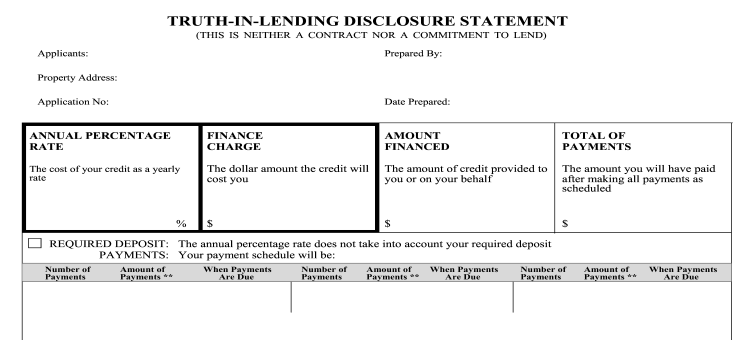

TILA

Reg Z requires that a borrower be provided with a summary of the loan terms and financial impact. Below is a sample of the mandated Truth In Lending Agreement or disclosure form:

Credit Reporting

The Fair Credit Reporting Act (FCRA) requires that loans be accurately reported to a Credit Reporting Agency (CRA) more commonly know as Credit Bureaus. Mbanq reports the Platform's credit and lending products to the three main U.S. Credit Bureaus: Experian, TransUnion and Equifax.

Updated about 1 year ago