Secured Credit Cards

API References:

Mbanq Cloud's CORE capabilities empower fintechs and neo banks to launch Secured Credit Cards, offering numerous advantages for both banks and customers. From a bank's perspective, the ability to offer secured credit cards alleviates the burden of extensive credit review and underwriting processes. This means less stringent requirements for companies wanting to make cards available to their users. Secured credit cards are particularly beneficial for individuals with little to no credit history or those who seek better fund management. With a secured card, users have the advantage of knowing exactly how much they can spend without worrying about going over their limits.

From a Cardholder's perspective, secured credit cards provide several advantages. One key feature is the linkage between a Security Deposit Account (SDA) and the credit card. This connection allows for greater control and flexibility in managing funds. Additionally, the credit card's limit is set based on the balance available in the SDA, enabling Cardholders to make informed spending decisions in line with their financial means.

Security Deposit Account (SDA) Rules

- A Security Deposit Account is not the same as a regular Demand Deposit Account.

- Demand Deposit Account (DDA) - is what people normally think of when they same a bank account. The account holder cardholder may move money into and out of their DDA account at any time. Typically card access to a DDA account is done using a Debit card. A DDA account may not be used as security for a secured credit card.

- An issuer may not: Access, debit, hold, or settle funds from the consumer’s demand deposit or asset account.

- An issuer may not: Earmark, hold, or freeze funds in a customer’s general demand deposit or asset account as collateral. Any security deposit account needs to be pre funded prior to any transactions taking place.

- Any secured credit card program that attempts to access, debit, hold or settle funds less than 14 days after the purchase transaction would likely trigger the definition of a “Visa POS Debit Device” under the Walmart Settlement agreement.

- Security Deposit Account (SDA) - is typically a cash collateral account. The account holder as well as the bank may not move money into or out of the SDA. In addition, the account holder of an SDA assigns rights to the bank such that the bank has the ability to withdraw funds from the account without seeking card or account holder approval when the secured credit card account is in default.

- If a secured card includes a feature where funds move from the consumer’s deposit account into the SDA account, the issuer cannot be the person who determines when/how funds move in/out of the SDA account because it is possible that the issuer’s sweeping of funds from the consumer’s deposit or checking account into the SDA account would be considered a debit or hold that makes the product a POS Debit Device or Debit card.

- Demand Deposit Account (DDA) - is what people normally think of when they same a bank account. The account holder cardholder may move money into and out of their DDA account at any time. Typically card access to a DDA account is done using a Debit card. A DDA account may not be used as security for a secured credit card.

- The Cardholder must provide a security deposit in the local currency from a deposit account to secure

the obligations to the issuing bank or Platform that they may incur in connection with making purchases with their Secured Credit Card. - The Cardholder may not withdraw Funds from the Security Account unless their credit card account is closed and paid in full ($0 balance.)

- The Cardholder grants the issuing bank and Platform a security interest to all funds in the Security Deposit Account.

- The Cardholder irrevocably and unconditionally relinquishes possession and control over the SDA Collateral.

- The issuing bank or Platform can not withdraw funds from the SDA to make payment on the Secured Credit Card Account, unless the Secured Credit Card Account is in default.

- If the Cardholder is in default of any obligation under the Cardholder Agreement; or the Cardholder Secured Credit Card Account is closed for any reason, the Cardholder authorizes the issuing bank and or Platform to withdraw Collateral from the Security Account and apply such amounts to the Secured Credit Card Account without sending the Cardholder notice or demand for payment.

Fully Activated

Once the consumer has funds in their securing cash account, secured cards work just like unsecured ones:

- The user can use secured credit cards wherever credit cards are accepted, including online.

- The user's bill comes monthly, and the user can pay for the purchases they have made. (Their deposit is not used to pay for purchases, it is only used when the user defaults on making their payment)

- The user will incur interest on the outstanding balance.

- User can build or rebuild their credit by using the card responsibly and paying their balance on time.

By leveraging Mbanq Cloud's CORE capabilities, fintechs and neo banks can effectively introduce secured credit cards, providing customers with a valuable tool to build credit, manage their finances responsibly, and enjoy the benefits of credit card usage.

Business Set Up

There are a number of business action items that need to be completed to obtain approval for launching a credit program with Mbanq and a Partner Bank. These action items fall into the following main categories:

Application

- Application for Credit Card program

- Compliance Review

- Underwriting procedure and model

- Credit Committee Charter

- Marketing materials

- Adverse Action Notices and other communication templates

- Collections policy

- Application and origination screen flow

- Servicing screen flow

- Disputes process

- Submission to Partner Bank

- Approvals

- Register Card BIN (Bank Identification Number) with the Visa Network

- Print and ship physical cards to end users (if requested)

- Fund the required credit and reserve accounts as per the agreements

Credit and Reserve Account Funding

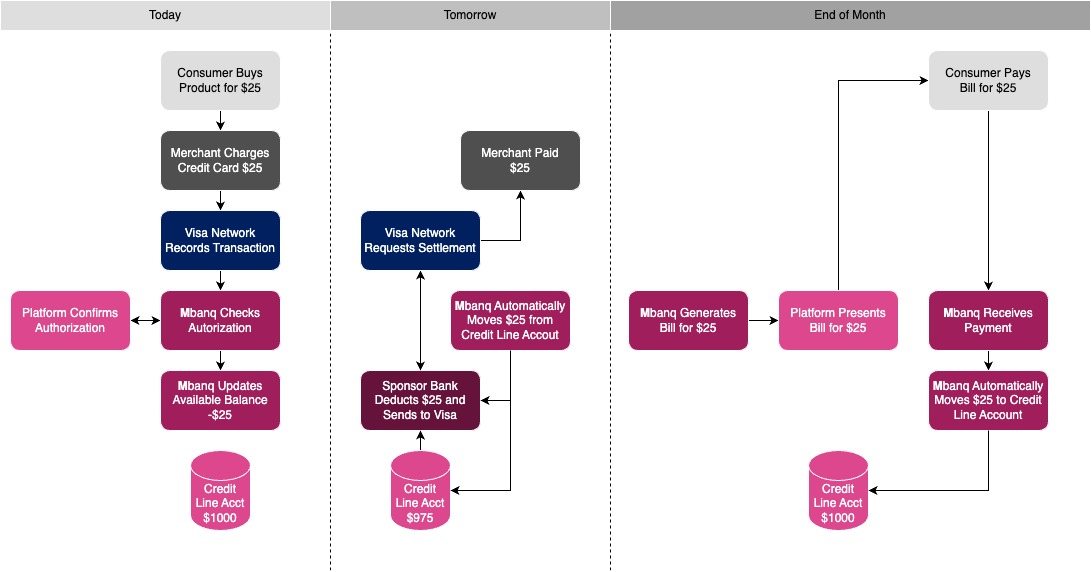

The credit risk for the credit extended to the consumer or business is the responsibility of the Platform. The Platform will have to establish and fund two main accounts:

- Credit Line account - these funds are set aside and represent the total amount of credit that the Platform can extend to its customers at any given time. This credit line account gets replenished when the customer makes the payment against the total outstanding balance on their account.

- Reserve account - this reserve account covers other delinquencies such as unpaid fees, unpaid invoices for card printing, etc.

Product Set Up

In order to enable customers to use their secured credit cards, your Platform will have to integrate with Mbanq's APIs.

- Begin by setting up the Secured Card product via the Mbanq console (Credit Card Product Setup)

- Create a new secured credit card product for your platform instance

- Be sure to select Secured for the account type and link the securing account

- Set the authorizations and rate limits

- Build integrations with the following Mbanq APIs:

- Accounts (Create Account) Create consumer users and their associated bank and credit accounts - this account product should be pre-configured to not allow any debits / withdrawals from the SDA account.

-

- Credit Cards

- Create Card (Create Card) Create a new card instance

- Issue a New Card (Issue a New Card) Issue a virtual or physical card

- Approve Credit Card (Approve Credit Card) Approve and authorize a card for use

- List Transactions (List Transactions) Return a list of all the card transactions for a date range

- Get Transaction Details (Get Transaction Details) Return the details for a specific transaction

- Retrieve a Statement (Retrieve a Statement) Return PDF or JSON version of a card account statement

- Make a Payment (Make a Payment) Card account payment internal or via ACH

- Adjust Card Limits (Adjust Card Limits) Change the limit and velocity caps for a specific card account

- Dispute a Transaction (coming soon)

- Card Issuing

- Toggle Card Features (Toggle Features) Turn on and off various card features

- Suspend Card (Suspend) For non-payment or if lost or stolen

- Terminate Card (Terminate) When an account is closed or when fraud is confirmed

Updated about 2 months ago